Let’s get into the fundamental factors which have an impact on the key currencies. Get ready for some economics!

USD

US central bank is still expected to raise interest rates in December and by doing so the Fed will tighten monetary policy, unlike many other major central banks. However, the next month’s rate increase is already priced in the USD exchange rate. As a result, the greenback is no longer able to get substantial positive drivers from it. Traders are more interested in what the Federal Reserve will do the next year. The latest change in their outlook was bearish for the USD. According to the new estimates, the pace of the Fed’s rate increases in 2019 will be slower than it was thought before (only 1 rate hike is currently foreseen). The switch in expectations happened after the Fed’s Chair Jerome Powell said on Wednesday that the central bank’s policy rate is now “just below” estimates of a level that neither brakes nor boosts a healthy American economy. In addition, minutes from the Fed’s November meeting showed that the Fed members started discussing when to pause further hikes and how to communicate this pause to the market. All this led to a pause in the bullish momentum for the USD.

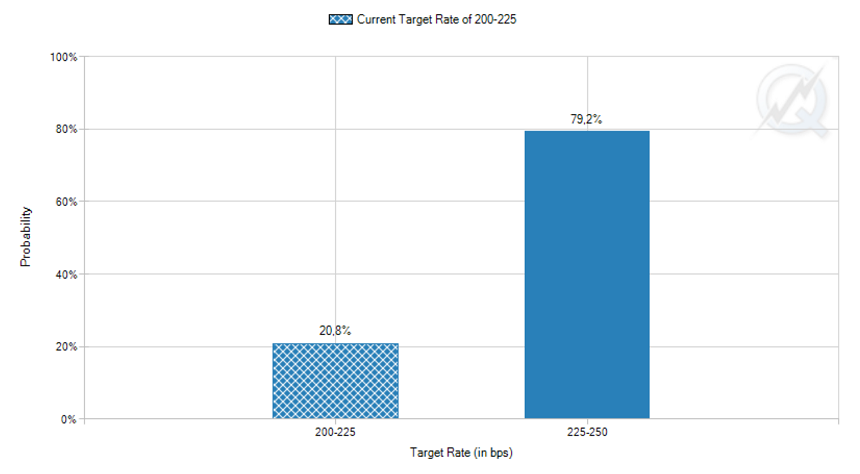

The probability of the Fed's rate hike on December 18 is estimated by 80%, according to futures on federal funds rate

The latest economic figures weren’t rosy. Data from the United States showed that data showed that inflation slowed in October (core PCE price index rose by only 0.1% vs. the 0.2% growth in September), despite a jump in consumer spending by 0.6% due to the increased spending on prescription medication and utilities.

The USD may enjoy the external demand as a safe haven if trade talks between Donald Trump and his Chinese counterpart fail on Friday and Saturday. On the other hand, if the United States and China schedule another meeting to discuss trade and sound optimistically, the USD will decline versus the riskier currencies like the AUD and the NZD.

EUR

Fundamentals for the single currency don’t look bright. GDP growth declined by half in Q3 to only 0.2% q/q, while Germany, the largest economy of the region, even contracted by 0.2%. European November PMI disappointed indicating that trouble is spreading in the final months of the year. Finally, flash consumer inflation weakened. Headline CPI growth decreased from 2.2% to 2.0%. The fall in oil prices must have contributed to inflation's slowdown.

The European Central Bank is expected to end QE purchases in December as planned. The regulator’s meeting on December 13 will draw great attention. Declining inflation pressures can make the ECB sound dovish and make the EUR float down.

Political pressures are still present as well. Italian authorities said that they can adjust the budget deficit by 0.2% down to 2.2% but wouldn’t yield more. As the figure is still above EU's Commission 2.0% target, tensions will likely continue.

All mentioned above allows assuming that the EUR doesn’t have a lot of strength of its own. Take this into account when trading.

GBP

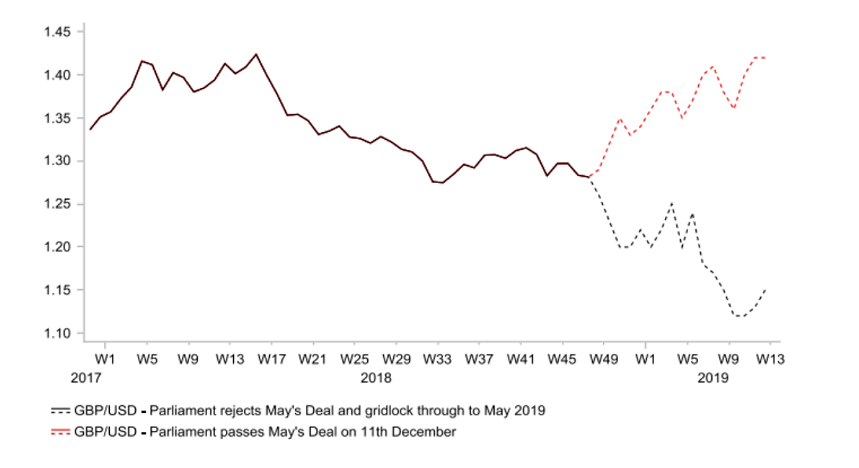

The talk about the GBP has to start with Brexit. Although progress has been made between Britain and the European Union, everyone is now worried about the UK parliament's vote on Brexit. The choice is between Prime Minister Theresa May's proposals and a no-deal Brexit. The parliamentary opposition to May’s agreement with the EU is strong. If her proposal fails in the parliament on December 11, there can be no doubts that the GBP will go to new much lower ranges.

The Bank of England warned that if Britain leaves the European Union in a disorderly manner, the GBP would crash, inflation soar, interest rates would have to rise and Britain’s growth would plummet.

Forecasts for GPP/USD by analysts at MUFG

Already British economy isn’t doing very well either. Retail sales fell by 0.5% in October, preliminary business investment dropped by 1.2% in Q3, services and manufacturing PMI keep showing lower numbers. Although GDP growth accelerated in Q3, it was null in September. So, mark the GBP as having the potential to heavily depreciate.

JPY

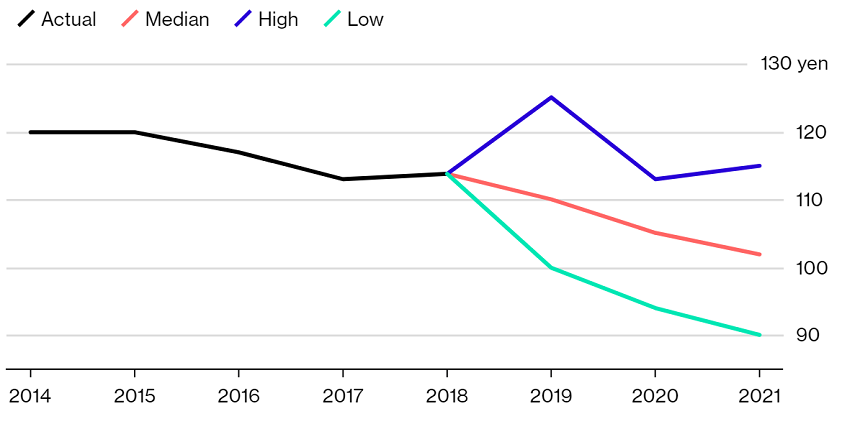

According to a Bloomberg survey, the Japanese yen will strengthen during the next couple of years. So far traders were not really interested in the Bank of Japan but now analysts start expecting some policy tightening. Low interest rates are bad for the Japanese banking sector in the long run, so the BOJ may be forced to become more hawkish. The steps probably won’t be radical and just involve greater flexibility in Japanese government bond yields, but together with slower rate hikes by the US Federal Reserve, this can give a boost to the JPY.

The latest survey about the future value of USD/JPY done by Bloomberg

There were some positive developments in the Japanese economy to back this scenario. The nation’s retail sales jumped by 3.5%, the highest level since December 2017. At the same time, Japanese inflation remains weak, far below the BOJ 2% target. This means that the hawkish BOJ story will have to wait for some time. In the medium term, the dynamics of the JPY will depend more on investors’ risk sentiment: up if they are averse to risk and down if everyone becomes optimistic. Trade wars, Brexit and Italy’s debt are the main topic affecting the overall risk appetite.

AUD

Another currency which is highly dependant on risk sentiment is the AUD. Bulls are keeping their fingers crossed for the meeting between Mr Trump and Mr Xi to go well.

Disappointing data from China, Australia’s main trading partner is not helping the Aussie. Australia’s own private capital expenditure contracted. The regular meeting of the Reserve Bank of Australia will take place on December 4. No changes in monetary policy are expected as lower oil prices put a drag on inflation. If the RBA comments on the recent rebound of the AUD, the currency will get hit.

In addition, don’t miss Australia’s GDP on December 5 and retail sales on December 6. Australian economic growth will likely be healthy, although household consumption is limited by high debt. So, the AUD doesn’t have really good drivers on its own. For the rally to continue, there should be some really good news about the US-China trade issue.