AUD: long-term outlook

Tactical rise

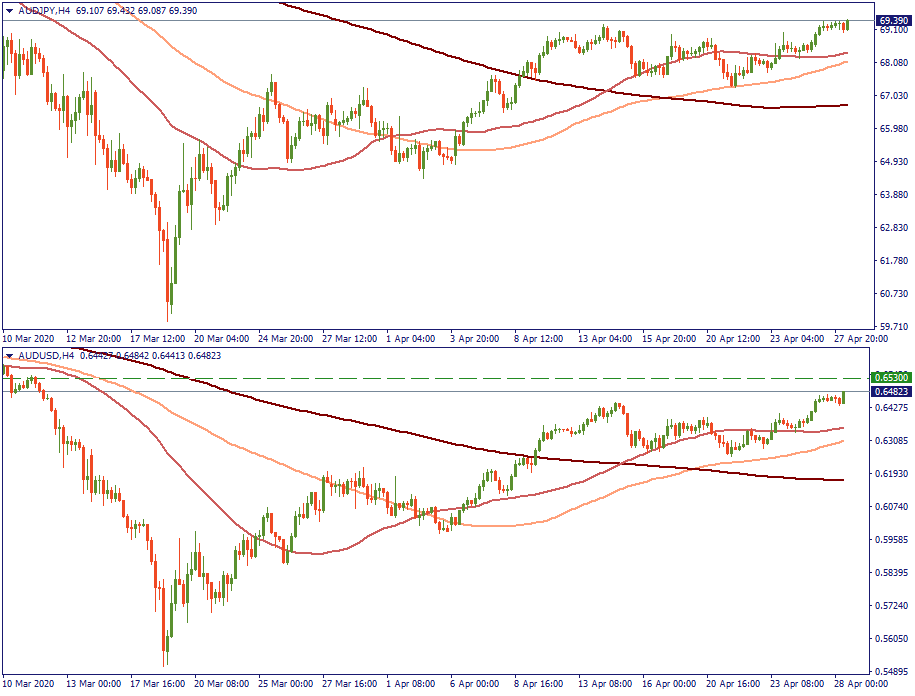

The Australian dollar has been doing pretty well lately. Specifically, the last 6 weeks give an almost identical picture for its performance against the USD and JPY. Observers recognize the strong behavior of Aussie mostly explaining it by the fact that the Chinese economy is already on a steady recovery path “dragging” the Australian economy out of the bottom with it. That is just a tactical picture, however. What is the strategic layout?

Strategic decline

For the last two years, the Australian dollar has been going down against the USD. In fact, is has been in decline against the US dollar since 2011, with only one big change that took place during 2016-2017. As the monthly chart shows, where the currency pair is currently is where it in 2009 before it started its ascension. In other words, at 11-year lows. On that monthly chart, the very last green candlestick represents these last weeks of rising that we have observed lately. Not very impressive on a grand scale. Or is it? Let’s dig into fundamentals to see what’s coming for the Australian dollar.

Fundamentals

The sunny side has a few things to mention. First, due to close trade tides with China, Australia is one of the first economies that has started recovery. However, It is important to recognize the correct interpretation of this indication: the fact that the AUD is on the rise since the middle of March reflects good timing, not good recovery. Second, an extensive stimulus package is helping businesses and families to stay afloat and ignite the dormant economic mechanisms. So the RBA is doing its part to make sure things are as good as they can under these conditions. And third, Australia managed the virus pretty well. It could have been much worse for the country. Therefore, not all is lost.

The gloomy side, however, has some heavy factors to mention. First, the scale of economic contraction is going to be the biggest since the Great Depression. The GDP is expected to keep shrink until the end of this year, with a prognosis to reach the pre-virus levels only in 2022. That means the coming two years are going to be tough anyway. Second, there was certain consumer overspending in the first quarter of this year, which will lead to underspending in the second quarter dragging consumer activity even lower. Third, there is a risk of virus re-occurrence in the next year. Although that’s not something Australia-specific, the country does have this risk in front of it as well.

For the AUD, therefore, we the following layout. The labor market will hardly be in a position to approach full employment this year. Raising the interest rate is therefore ruled in the nearest future – at the very best. Therefore, the correct question for the AUD is not how high it may rise against the basket of currencies, but how stable it may be throughout this year, while Australia is still discovering the full scale of the virus damage.